As we head towards the finish line of the 2024 financial year on 31 March, you may be thinking about preparing for your end of year stocktake, writing off any bad debts from your Accounts Receivable ledger, or setting some goals for the year ahead. There are a few proposed changes that are likely to take effect from 1 April 2024 that we thought would be good for you to be aware of. Some of these changes are currently included in a bill before Parliament and are expected to be reported on by the end of March 2024.

Increase in Minimum Wage

The adult minimum wage will be rising from $22.70 to $23.15 per hour from 1 April 2024. For an employee who works 40 hours per week on the minimum wage, the increase will mean they will earn an extra $18 per week before tax (which is an increased cost to the employer).

Increase in the Trustee Tax Rate

While it is not yet law, the Government has proposed to increase the Trustee tax rate from a flat 33% to 39% from 1 April 2024 (effective for the 2024/2025 income tax year). At the current tax rate of 33% it is thought that some individuals can obtain a tax advantage by earning income through a Trust, as this allows them to avoid the 39% personal tax rate. The increase would align the trustee tax rate with the top personal tax rate of 39%, for personal income over $180,000.

The Finance Minister, Nicola Willis has revealed the Government intends to modify the current bill to exempt some trusts from paying the increased tax rate, through certain carve outs and a de minimis rate, although little detail has been shared at this point.

A couple of the suggested exceptions include where a deceased person’s affairs are still being settled, the estate (which is taxed as a Trust) may be allowed to apply the deceased’s personal tax rates for a period of 12 months. Certain Trusts that have been settled for disabled people may be allowed to have the trustee income taxed at the disabled beneficiary’s personal tax rate.

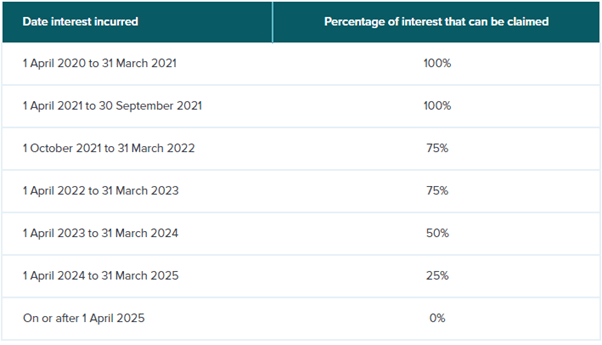

Interest deductibility on Residential Rental Property

The Governments press release in December 2023 announced their commitment to fully restore the interest deductibility for residential rental properties.

The previous Government had introduced a plan to phase out the deduction of interest against rental income derived by residential landlords, resulting in landlords having to pay more income tax. For properties acquired on or after 27 March 2021 interest could not be claimed as an expense in the calculation of profit for tax purposes (unless an exclusion or exemption applied). The ability to deduct interest on properties acquired prior to 27 March 2021 was to be phased out as follows:

There were some exceptions to the interest deductibility rules such as newly build properties and social housing, which maintained the ability to claim 100% of interest costs as a deduction.

The proposed changes to the interest deductibility rules are:

It is expected that the proposed changes will be backdated to 1 April 2023 and so will take effect for the 2023/24 income tax year. The phasing back in of interest deductibility would see 100% deductibility restored by the 2026 income tax year.

Interest deductions that were not allowed for the 2021/22- and 2022/23-income tax years will remain non-deductible.

Brightline Test for Residential Property

The Government press release in December 2023 also announced their decision to reduce the Brightline test for residential property back to two years. The current Brightline test requires property owners to pay income tax on property sold within a certain time frame:

The bright-line property rule looks at weather the property was acquired:

on or after 27 March 2021 and sold within 5 years for qualifying new builds or within 10 years for all other properties

between 29 March 2018 and 26 March 2021 and sold within 5 years

between 1 October 2015 and 28 March 2018 and sold within 2 years.

There are some exclusions from the bright line rules, for example, your main home, or where you receive roll-over relief on the transfer of a property.

It is proposed that the Brightline test will reduce to two years, effective from 1 July 2024.

This would mean that properties sold after 1 July 2024 will only be subject to tax under the Brightline test if they are sold within two years, regardless of when they were purchased.

Depreciation on Commercial Buildings

The ability to claim depreciation on buildings has changed multiple times over the years – up until 2010 depreciation was allowed on most buildings; for the 2012 – 2020 income years the depreciation rate for buildings with an estimated life of more than 50 years was set at zero; from the 2021 income year depreciation deductions were reintroduced for non-residential buildings.

The Governments mini budget is set to remove the deduction once again for depreciation on commercial buildings. It is expected that this would be implemented from 1 April 2024, so would apply for the 2024/25 income tax year.

We hope the 2024/25 year starts well for you and look forward to updating you on the proposed changes as they become available.